Embedded Coverage vs Traditional Protection: What Businesses Need to Know

The moment a customer clicks away from your platform to buy protection is the moment you lose control. Traditional refund protection often forces this redirect, costing businesses both revenue and trust. But there's a better way.

Embedded coverage represents a $10 billion global market opportunity, projected to grow nearly four times by 2030. This isn't just about adding a feature—it's about fundamentally rethinking how protection fits into the customer journey. While traditional protection tends to pull customers out of your experience, embedded coverage keeps them exactly where they should be: on your platform, in your flow, completing their purchase with confidence.

The difference between these models isn't cosmetic. It's structural, technical, and financial. Let's break down what businesses evaluating protection options need to understand.

What is Embedded Coverage?

Embedded coverage means integrating financial protection directly into your product or service at the point of purchase—no redirects, no third-party handoffs, no friction. The customer stays on your platform from browse to book.

Think of it as protection woven into the purchase experience rather than bolted onto it. When someone books a ski pass, registers for a marathon, or reserves concert tickets, they can seamlessly add coverage in the same flow. The interaction feels native because it is native.

For platforms and SaaS businesses, this isn't just about customer experience—it's about economics. Research from Deloitte's embedded finance analysis shows that SaaS businesses leveraging embedded finance can increase revenue per user by 2 to 5x, making it one of the most impactful ways to drive growth without acquiring new customers.a

Examples across categories:

- Event Ticketing: Refund protection added at checkout for concert tickets, letting customers cancel for any reason

- Ski Resorts: Season pass protection that adjusts based on pass type and coverage preferences

- Tour Marketplaces: Cancel for any reason coverage integrated into multi-day adventure bookings

- Booking Platforms: White-label protection that SaaS platforms can offer their operator clients

These embedded refund solutions go by different names—cancel for any reason coverage, embedded checkout protection, refund protection. Our solution, Refund Guarantee, delivers the same core value: native integration, flexible design, and frictionless customer experience.

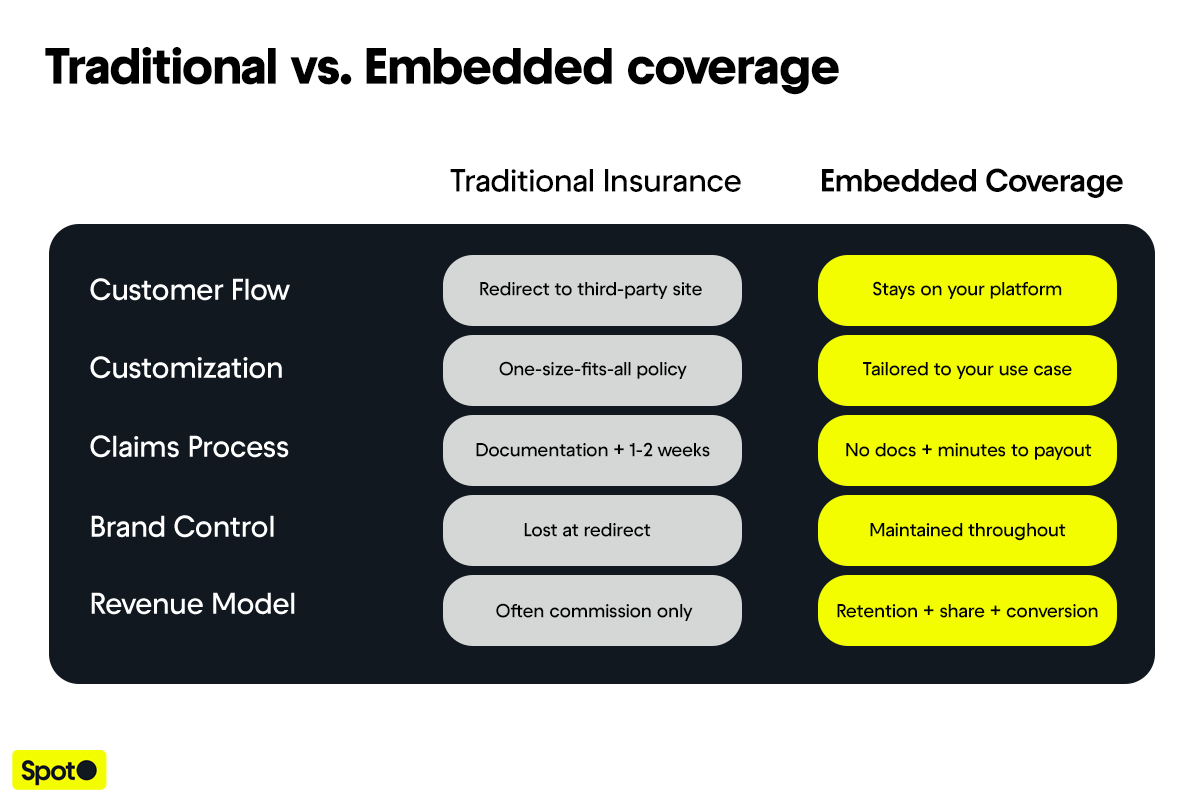

Here's the fundamental difference visualized:

The Traditional Protection Problem

Traditional refund protection models were built for a pre-digital world. The cracks are showing.

The Redirect Tax

When customers leave your platform to evaluate or purchase protection, you're playing with fire. Research shows conversion rates can drop 30-50% at redirect points. Every click away is a chance for hesitation, comparison shopping, or simple abandonment.

More critically, you lose brand control the moment they land on a generic insurance site. The trust you've built? It doesn't transfer. The experience you've crafted? It ends. Your customer is now navigating someone else's forms, reading someone else's fine print, and making decisions in someone else's ecosystem.

Even solutions marketed as "embedded" can fall into this trap. If the coverage offering feels like a generic widget dropped into your checkout—mismatched design, insurance jargon, clunky flows—you've avoided the redirect but kept the friction. The customer stays on your platform, but the experience still feels foreign.This is why true embedded coverage goes beyond technical integration. It's about making protection feel native: matching your brand, speaking your customer's language, and presenting coverage as a natural part of the purchase—not an insurance product bolted on.

The Rigidity Trap

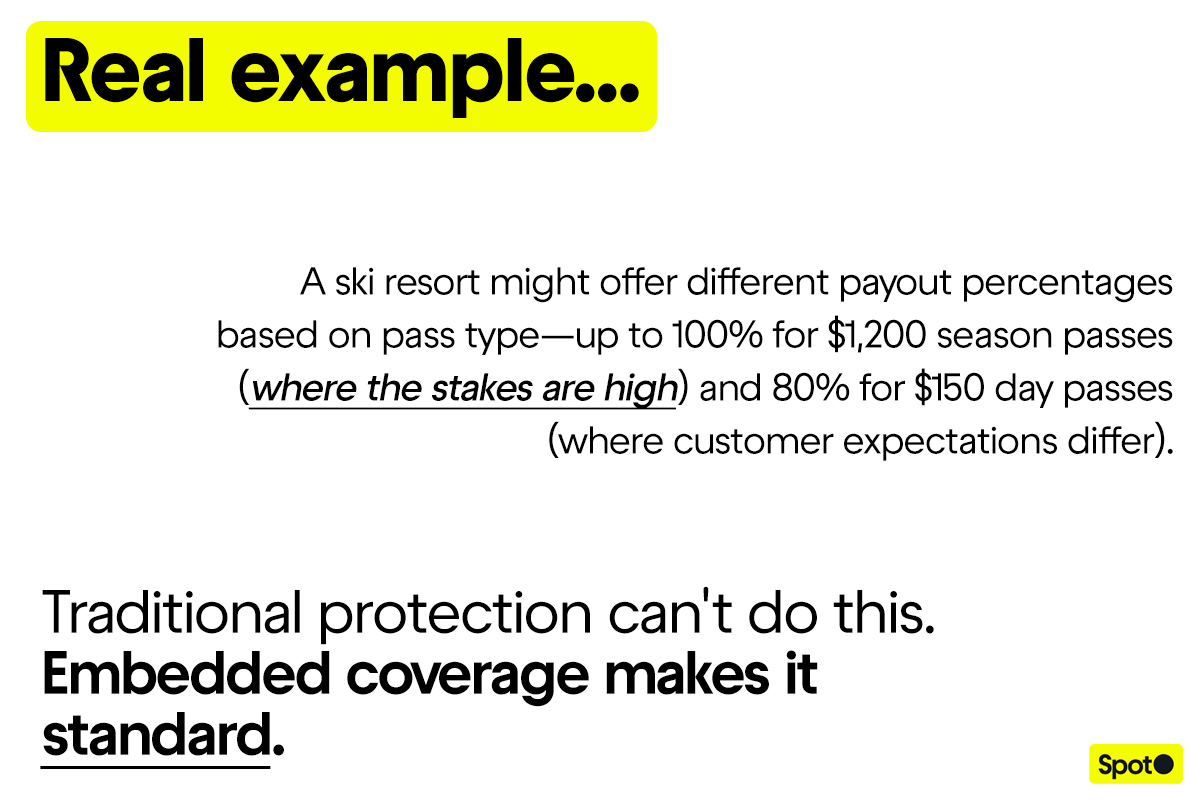

Traditional refund protection products are designed for scale, which means they're designed to be generic. A ski resort can't get different coverage terms for day passes versus season passes. An event platform can't adjust refund percentages based on how far in advance tickets were purchased.

Want to customize? Get in line. Traditional insurance partnerships take months to modify because they're built on decades-old infrastructure with complex approval chains. Your business moves fast; their product design doesn't.

The Customer Friction

Even after customers buy traditional protection, the pain continues. Filing a claim often requires:

- Documented proof of why they're canceling

- Medical certificates, weather reports, or other official documentation

- Forms filled out in triplicate

- 1-2 week processing times (or longer)

- Phone calls, email exchanges, and general frustration

For purchases under $1,000, this hassle often isn't worth it. Customers simply abandon the claim process altogether, losing both their money and their trust in the protection they paid for.

For a generation that expects Amazon-level service, this experience feels broken. According to Bain Capital research, 80% of younger consumers prefer protection integrated directly into digital platforms—not bolted on through clunky third-party processes.

How Embedded Coverage Works Differently

Modern embedded coverage solves these problems through three core principles: flexibility, simplicity, and technology.

Built for Flexibility

Embedded coverage solutions are designed to mold to your business model, not force you into theirs.

Want to offer 90% refunds for premium bookings but 80% for standard? Done. Need different coverage windows based on how far in advance someone books? Configured. Prefer to include protection in the price versus offering it as an add-on? Either works.

This flexibility extends to optimization. The best embedded coverage platforms support A/B testing, letting you experiment with different price points, benefit structures, and checkout presentations. Traditional insurance partnerships might let you change pricing once a year if you're lucky. Embedded coverage lets you iterate based on your needs and what the data tells you.

Designed for Simplicity

Simplicity works on two levels: operational simplicity for you, experiential simplicity for your customers.

For your business:

- API-first integration means your engineering team connects once and you're live

- Minimal operational burden because your partner handles claims, customer service, and payouts

- Real-time dashboards show exactly how the program is performing—attachment rates, utilization, net revenue

You're not building an insurance operation. You're integrating a solution.

For your customers:

- No fine print maze to navigate—coverage is straightforward and easy to understand

- No documentation required to file a claim (cancel for any reason means exactly that)

- 2-3 minute claim process followed by payout in under 10 minutes, not 10 days

Traditional protection averages 1-2 weeks for payouts. Embedded coverage averages minutes. That's not an incremental improvement—it's a completely different customer experience.

Powered by Technology

The "how" behind embedded coverage's flexibility and simplicity is modern technology infrastructure.

Native integration: True embedded solutions use SDKs and APIs that make the protection offering feel like it's built directly into your platform—because it is. No iframes. No white-labeled third-party pages. Native components that match your design system.

Checkout optionality: Different businesses need different presentation models. Some want an embeddable widget in the cart. Others want to present protection as a "refundable vs. non-refundable rate" choice earlier in the booking flow. Embedded coverage platforms support both.

Logic-driven refunds: When a customer requests a refund, the system checks eligibility automatically based on pre-set rules. No human adjudication. No claims team reviewing documentation. If they're within the coverage window and canceling for any reason (which is the point), the refund processes instantly.

This technological foundation is what makes 2-4 week integrations possible.

The Business Impact

Here's where embedded coverage gets interesting financially.

Refund Guarantee (and embedded coverage solutions like it) allows for:

- Revenue retention: When a customer cancels, your embedded coverage partner issues the refund—you keep the original booking revenue

- Revenue share: You earn a portion of the coverage price as the distribution partner

- Conversion lift: Offering flexible cancellation options increases initial purchase conversion because customers book with confidence

- Price optimization: Find the right price (and conversion mix) to drive more revenue through A/B testing

- Inventory resale: You can re-sell cancelled slots, effectively earning revenue twice on the same inventory

We'll explore the detailed ROI math in a future deep-dive, but the directional insight is clear: embedded coverage turns cancellation risk into revenue opportunity.

Industries Benefiting from Embedded Coverage

Embedded coverage isn't limited to one vertical. Any business with advance bookings and cancellation risk can benefit.

Marketplaces

OTAs and tour aggregators face a unique challenge: they aggregate inventory from hundreds or thousands of suppliers, each with different refund policies. Traditional protection can't accommodate this variability. Embedded coverage creates a uniform protection layer across all suppliers, giving customers consistency and giving the platform control over the experience.

Recreation Venues

Ski resorts, theme parks, and attractions deal with weather dependency and variable attendance. A season pass purchase in October for winter skiing carries inherent uncertainty. Cancel for any reason coverage removes that friction, encouraging earlier purchases and larger commitments. When customers know they're protected, they're willing to commit sooner.

Event Ticketing & Experiences

Concert tickets, marathons, and festivals are typically non-refundable to prevent scalping and ensure revenue predictability. But rigid policies hurt conversion—especially for events booked months in advance. Embedded coverage offers the best of both worlds: operators keep revenue predictability, customers get flexibility, and the conversion funnel improves.

Booking Platforms (Vertical SaaS)

SaaS platforms serving tour operators, activity providers, or venue managers can differentiate by offering white-label embedded coverage as a platform feature. Their clients (individual operators) get access to sophisticated protection solutions they couldn't build themselves, and the platform earns revenue share on every policy sold through their system.

Choosing an Embedded Coverage Partner

Not all embedded coverage solutions are created equal. Some are just traditional protection with better marketing.

Red flags to watch for:

❌ White-labeled traditional products: If the underlying product is still a standard insurance policy with all the usual restrictions, embedding it doesn't solve the core problems

❌ Multi-month integration timelines: If implementation takes half a year, the infrastructure isn't truly modern

❌ You handle customer service: The operational burden should shift to your partner, not stay with you

❌ Rigid structures: If you can't customize coverage terms for your use case, it's not really flexible

Green flags to look for:

✅ API-first architecture: Modern infrastructure that integrates in weeks, not months

✅ Flexible product design: Ability to customize payout percentages, coverage windows, and pricing to match your business model

✅ Full-service support: Your partner handles claims, customer service, and payouts end-to-end

✅ Real-time analytics: Dashboards that show attachment rates, utilization, and performance metrics as they happen

✅ Multi-vertical experience: Partners who understand different use cases beyond just travel and event ticketing bring more valuable insights

✅ True partnership approach: The best relationships include hands-on help with program design, pricing strategy, and optimization

💡The right embedded coverage partner doesn't just provide technology—they become an extension of your team, bringing expertise in customer experience, program economics, and continuous optimization.

FAQs About Embedded Coverage

Is embedded coverage the same as traditional travel insurance?

No. Traditional travel insurance requires customers to leave your platform, covers only specific reasons (illness, weather events, etc.), demands documentation for claims, and takes 1-2 weeks for payouts. Embedded coverage stays native to your platform, covers any reason the customer wants to cancel, requires zero documentation, and processes refunds in minutes. The customer experience is fundamentally different.

Won't offering cancel for any reason protection cause excessive cancellations?

Industry data shows typical utilization rates of 50-60%, which means these programs are profitable when priced correctly. More importantly, offering this flexibility increases initial conversion because customers book with greater confidence earlier in their planning cycle. You're not just preventing cancellation losses—you're driving more bookings upfront.

Do we need insurance licenses to offer embedded coverage to customers?

No. When you partner with an embedded coverage provider, they handle all regulatory compliance and licensing requirements. You're simply integrating their solution into your platform—similar to how you'd integrate a payment processor or booking engine. The regulatory burden stays with your partner.

How long does integration typically take?

With an API-first partner and modern infrastructure, standard integrations take 2-4 weeks. Complex customizations might extend to 6-8 weeks. Compare this to the 3-6 month implementations typical of traditional insurance partnerships, which often require extensive back-and-forth, legal reviews, and legacy system accommodations.

Can the coverage be customized for our specific business model?

Yes—customization is one of embedded coverage's core advantages. Payout percentages, coverage windows, pricing structures, and even checkout presentation can all be tailored to your use case. A ski resort needs different terms than a concert venue, and both need different terms than a marathon registration platform. Traditional one-size-fits-all products can't accommodate this. Embedded coverage makes it standard practice.

What's the revenue opportunity for our business?

Partners typically earn a revenue share on coverage sales. But that's just one revenue stream. You also retain booking revenue when customers cancel (instead of refunding it), and you can re-sell cancelled inventory. The combination of these three revenue streams—share, retention, and resale—often turns cancellations from pure loss into net positive outcomes. The exact economics depend on your pricing, attachment rates, and utilization rates.

Are there geographic restrictions on where we can offer embedded coverage?

No. Unlike traditional insurance products that require separate policies and regulatory approvals for each country, Refund Guarantee operates without geographic restrictions. Whether you're serving customers in the US, Europe, Asia, or expanding into new markets, the same solution works everywhere. This flexibility means you can scale internationally without the typical insurance compliance burden slowing you down.

Embedded coverage isn't traditional protection with a modern interface. It's a fundamentally different model built for how businesses and customers actually operate today.

Whether you're a booking platform managing diverse supplier inventory, a venue operator dealing with weather uncertainty, or a SaaS provider looking to add value for clients, embedded coverage offers a path to turn cancellation risk into revenue opportunity.

The question isn't whether embedded coverage works—the data is clear. The question is whether your current protection approach is helping or hurting your business.